|

cyberbarf VOLUME 13 NO. 9 EXAMINE THE NET WAY OF LIFE APRIL, 2014

THE COIN OF THE NEW REALM THE ABANDONMENT OF AMERICA'S IDEAS BARFETTES iTOONS WHETHER REPORT NEW REAL NEWS KOMIX! SHOW HACK!

|

|

cyberbarf EXAMINE THE NET WAY OF LIFE

QUICK & RELIABLE SERVICE

CYBERBARF T-SHIRTS, MUGS & MORE

THANK YOU FOR YOUR SUPPORT!

CYBERBARF

PRICES TO SUBJECT TO CHANGE PLEASE REVIEW E-STORE SITE FOR CURRENT SALES

|

|

|

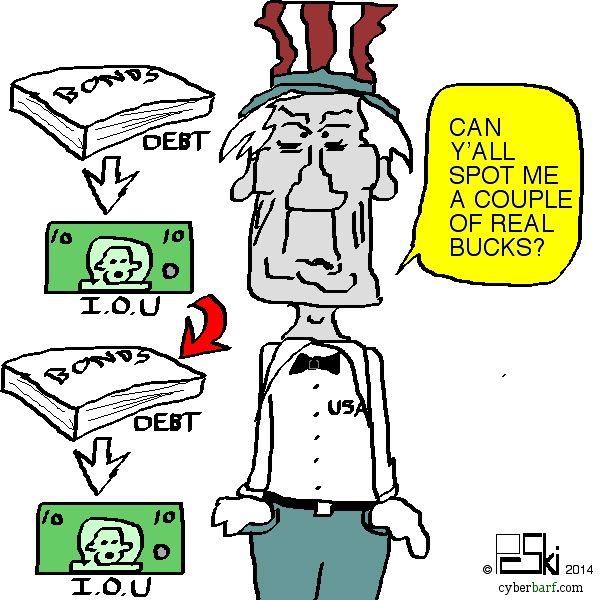

cyberbarf EXAMINE THE NET WAY OF LIFE cyberbarf THE COIN OF THE NEW REALM ARTICLE Much has been made of cybercurrency as a possible replacement to traditional currency. It seems like a simple statement, but the concept of money has a long and complex history. The current clearing exchanges of money make it difficult to use digital payments for all transactions. And those who currently control the monetary system will not be eager to let it go. Money is a commodity accepted by general consent as a medium of economic exchange. It is the medium in which prices and values are expressed; it circulates from person to person and country to country, thus facilitating trade, and it is the principal measure of wealth. The concept of money occupies a central place in economic theory. Money's form, shape, or substance is of relatively little significance (although convenience of handling and measurement is an important factor); its more crucial characteristic is that it is commonly accepted in payment for other goods and services. Throughout history a large number of commodities have been used as money (including seashells, beads, stone disks, and cattle), but since the 17th century the most common forms have been metal coins, paper notes, and bookkeeping entries. In standard economic theory, money is held to have four distinct but interrelated functions: (1) to serve as a medium of exchange, a commodity universally accepted in exchange for goods and services and for the discharge of debts or contracts; (2) to act as a measure of value and a unit of account, a common yardstick that makes the operation of the price system possible and provides the basis for keeping accounts and calculating cost, profit, and loss; (3) to serve as a standard of deferred payments, the unit in which loans are made and future transactions are fixed. Without money there would be no commonly accepted basis for borrowing and lending, and the concept of credit could not play the significant role in the economy that it does; and (4) to provide a store of wealth, a convenient form in which to hold any income not immediately required for use. This asset function of money provides a reserve of ready purchasing power. Money is the only completely liquid asset (that is, one readily convertible into other goods). Metals, especially gold and silver, have been used for money for at least 4,000 years. For perhaps 2,600 years, standardized coins have been the form in which money metals circulate. Gold and silver coins contain legally specified amounts of gold or silver and are theoretically equal in value to that quantity of the metal. Coins or uncoined bullion, however, can be an inconvenient and insecure mode for conveying large quantities of value. For large transactions, various forms of paper notes may be used to represent promises to pay in gold or silver. In the late 18th and early 19th centuries, banks began issuing such notes--banknotes--to represent convenient denominations of money. Each banknote was redeemable for gold or silver. This fiduciary money--money consisting of promises to pay in another medium--became the principal money of growing industrial economies. Eventually, for a variety of practical reasons, the circulating coinage began to be made of base metals, also taken to represent gold or silver on deposit somewhere and available on demand. Temporarily during World War I and permanently from the era of the Great Depression of the 1930s, the gold standard was abandoned by most nations, meaning that paper money was no longer convertible to gold on demand. Paper money issued on the general credit of a nation and not based on deposits of money metal is often called “fiat money.” To most individuals, money consists of coins, banknotes, and the amount of readily usable deposits held in banks and other financial institutions. As far as the economy is concerned, however, the total money supply is several times as large as the sum total of individual money holdings defined in this way. This is because a very large proportion of the deposits placed with financial institutions is loaned out, thus multiplying the overall money supply several times over. In fact, the money supply of a modern financial system includes a wide range of deposits, instruments of credit, and commercial bills. In this sense the best definition of money is by what it does: if an item is accepted as payment for goods, it can be regarded as money. The concept of money supply has come to play an increasingly important role in economic policymaking, because many economists believe that it is the quantity of money within the economy that ultimately determines real price levels, the rate of economic growth, and the rate of inflation. “Near money” refers to assets that, although not totally liquid, can be converted into cash at short notice, such as securities, insurance policies, and some building society loans. “Hot money” usually refers to funds that are moved from one country to another on a short-term basis in search of some temporary advantage. “Call money” is short-period loans made to banks that are repayable on demand. “Overnight money” denotes bank loans made each day and automatically repaid the following morning. One of the oldest, widely accepted functions of government is control over the supply of money. The dramatic effects of changes in the quantity of money on the level of prices and the volume of economic activity were recognized and thoroughly analyzed in the 18th century, and monetary economics has ever since constituted one of the principal branches of economics. In the 19th century a complex and somewhat crudely formulated tradition grew up known as the “quantity theory of money,” which held that any change in the supply of money can only be absorbed by variations in the general level of prices (the purchasing power of money). In consequence, prices will tend to change proportionately with the quantity of money in circulation. As the growth of fiat paper money gave governments increasingly effective control over the stock of circulating media, the quantity theory of money supplied an apparently simple rationale for the management of the economy: all that was needed to prevent inflation or deflation was to vary the quantity of money in circulation inversely with the level of prices. Economist John Maynard Keynes produced a different theory of the demand for money that implied that the impact of a change in the stock of money on the level of national income is weak and at best indirect; the effect on prices is virtually nil, he maintained, at least in economies with heavy unemployment such as prevailed in the 1930s. He put his emphasis instead on government budgetary and tax policy and direct control of investment. As a consequence, economists lost faith in monetary management and came to regard monetary policy as more or less ineffective in controlling the volume of economic activity. In the 1960s there was a remarkable revival of the older view, at least among a small but growing school of American monetary economists. They accepted much of Keynesian economics but argued that the effects of fiscal policy are unreliable unless the quantity of money is regulated at the same time. They refurbished the quantity theory of money and tested the new version on a variety of data for different countries and for different time periods, leading to the broad conclusion that the quantity of money does matter. In the late 20th century the controversy was still raging. It is notable that this debate, unlike previous debates in the history of monetary economics, was characterized by disputes over empirical findings--that is, it was focussed on the testable character of different monetary theories rather than on the manner of their formulation. Progress was made slower by the political overtones of the controversy: in some countries, belief in the efficacy of monetary policy had become a kind of litmus test of political conservatism. Nevertheless, a reconciliation between Keynesians and quantity theorists needed only some agreement as to the magnitude of monetary forces and the degree of stability of the demand for money. Monetary economics seemed at last to be coming of age as an empirical discipline. Monetarism is the school of economic thought that maintains that the money supply is the chief determinant of economic activity. (The money supply is the total amount of money in an economy, in the form of coin, currency, and bank deposits.) The American economist Milton Friedman is generally regarded as monetarism's leading exponent. Friedman and his adherents advocate a macroeconomic theory and policy that diverge significantly from those of the long-dominant Keynesian school. Their conservative approach became influential during the 1970s and early 1980s. Underlying the monetarist theory is the equation of exchange, which is expressed MV = PQ. M is the supply of money; V is the velocity of turnover of money (i.e., the number of times per year that the average dollar in the money supply is spent for goods and services); P is the average price level at which each of the goods and services is sold; and Q represents the quantity of goods and services produced. The monetarists believe that the direction of causation is from left to right in the equation; that is, as the money supply increases with a constant and predictable V, one can expect either an increase in Q with P remaining relatively constant or an increase in P if there is no corresponding increase in the quantity of goods and services produced. In short, a change in the money supply directly affects and determines production, employment, and price levels. Its influence, however, becomes manifest only over a long and often variable period of time. Fundamental to the monetarist approach is the rejection of fiscal policy in favor of a “monetary rule.” In A Monetary History of the United States 1867-1960 (1963), Friedman, in collaboration with Anna J. Schwartz, attempts to show that government intervention in the form of fiscal measures such as tax-policy changes or increased spending has no significant effect on inflation, deflation, or other fluctuations of the business cycle. Moreover, virtually all discretionary actions on the part of the government to alter the money supply aggravate the economy rather than stabilize it, since the conditions to which the authorities are responding have in most cases changed by the time their actions take effect. This is particularly true when the monetary authorities try to counter inflation or recession by modifying interest rates. Friedman contended that the government should seek to promote economic stability, but only by controlling the rate of growth of the money supply. It could achieve this by following a simple rule that stipulates that the money supply be increased at a constant annual rate tied to the potential growth of the gross national product (e.g., 3 to 5 percent). Monetarism thus posited that the steady, moderate growth of the money supply could in many cases assure a steady rate of economic growth with low inflation. Monetarism's linking of economic growth with rates of increase of the money supply was belied by the actual performance of the economy of the United States during the 1980s, however. By this time monetarist theory had become somewhat problematic. The proliferation of new and hybrid types of bank deposits obscured the types of savings that had traditionally been used by economists to calculate the money supply, and it also appeared that declining inflation and declining interest rates could further distort the money supply's predicted impact on economic growth. Economy theories on money and money supply get tossed about by economists and politicians all the time. Even though the two models seem to have nothing in common--the crucial variables of one do not even appear in the other--their descriptions of what happens during income level movements are not contradictory. Falling income is associated with an excess supply of goods and services in the income model, with an excess demand for money in the money model. Rising income is associated with an excess demand for goods in the first model, with an excess supply of money in the other. Evidently the two models give only partial descriptions of what is going on: one model looks at the process from the “real” side only and the other from the “monetary” side. But an excess demand for goods on one side will be associated with an excess supply of money on the other, and vice versa, so in this respect the two are consistent. The controversy between the two schools of thought represented by the models has mainly to do with two issues. One issue is which set of policy instruments--fiscal or monetary--provides the best means of stabilizing the economy. The other, more fundamental, issue concerns the causes of income movements. As seen above, changes in investment were the main cause of income movements in the income model; changes in the money stock were the main cause in the money model. Simplistic as the two models are, they embody the conflicting hypotheses of the two contending schools. Income-expenditure theorists attribute the instability of income primarily to events that influence the business sector's expectations with regard to the profitability of new investment, thus influencing investment. The modern quantity theorists see the irregular time path of the money stock as the most important factor. The gross features of economic history do not contradict either hypothesis. Private investment has indeed been the most volatile component of Gross National Product. Similarly, the movements of the money stock have conformed to those of money income: rapid inflation has been associated with a rapid growth of the money supply; severe recessions, with a decline in the money supply; and mild recessions, with a slowdown in the growth of the money supply. (“Mild” recessions may be thought of as recessions during which total employment stagnates, and the growth in unemployment, therefore, is largely due to the growth of the labor force.) The controversy has in large measure come to concern the direction of causation: one side maintains that shifts in investment cause income changes and infers that these in turn induce changes in the money stock which go in the same direction; the other side maintains that changes in the size or rate of growth of the money stock cause income changes that in turn will tend to fall most heavily on the investment component of income. The problem of resolving this controversy is twofold. First, the theoretical issue is less clear-cut than implied above. Each side acknowledges that neither investment nor the money supply is autonomous and that each affects the other. The question has become, therefore, which model is “most nearly true” and which model, consequently, should be regarded as a “first approximation” in guiding stabilization policy. Second, the empirical methods at the disposal of economists are not yet adequate for settling such issues. Attempts have been made to compare the performance of the two models by testing whether the best predictions of income are obtained by using actual data for “autonomous expenditures” and assuming that consumption will obey the consumption-income relation that has generally obtained in the past or by using actual money stock figures and assuming that money demand will obey the relation to income that has generally obtained in the past. These attempts have bogged down in disagreements on various statistical matters and must be judged inconclusive. They have shown, however, that even with consumption functions and money demand functions that are a good deal more “reasonable” than the naive relationships above, the predictions of both models are too inaccurate for the purposes of stabilization policy. Each model emphasizes one set of disturbances ("real" or "monetary", respectively) that will cause income to change. Each gives a partial view of the process of income-level movements. What is needed, therefore, is a third model explaining the linkages between “real” and “monetary” forces that these two simple models leave out. The general public has no concerns about economic monetary theories or the politics of public debt and the money supply. The public is really concerned with the day to day realities of living: earning money to buy life's necessities - - food, shelter, clothes, transportation, etc. Consumers know their individual purchasing power by the amount of bank notes in their wallets, the limits on their credit cards, and the numbers on their monthly financial statements. They know the effect of inflation when prices they pay for the same goods increase week to week. They understand that tax policy can take away take-home dollars needed to spend to support their households. The public holds its money as: (1) currency (including coin) and (2) bank deposits. In most countries the bulk of the currency consists of notes issued by the central bank. In the United Kingdom these are Bank of England Notes; in the United States, Federal Reserve Notes; and so on. It is hard to say precisely what “issued by the central bank” means. In the United States, for example, the currency bears the words “Federal Reserve Note,” but these notes are not obligations of the Federal Reserve Banks in any meaningful sense. The holder who presents them to a Federal Reserve Bank has no right to anything except other pieces of paper adding up to the same face value. The situation is much the same in most other countries. The other major item of currency held by the public is coin. In almost all countries this is token coin, worth as metal much less than its face value. So, it is the numbers printed on the money that is presumed value of bank notes and coins. Bank deposits are counted also as part of the money holdings of the public. In the 19th century most economists regarded only currency and coin as “money,” treating deposits only as claims to money. As deposits became more and more widely held, and as a larger fraction of transactions came to be effected by check, economists started to include not the checks, but the deposits they transferred, as money on a par with currency and coin. The definition of money has been the subject of much dispute. The chief point at issue is which categories of bank deposits to call money and which to regard as near money. Many economists include as money only deposits transferable by check (demand deposits). Others include nonchecking deposits, such as “time deposits” or “current deposits” in commercial banks. Still others include deposits in other financial institutions, such as savings banks, savings and loan associations, and credit unions. The term deposits is highly misleading. It connotes something deposited for safekeeping, like currency in a safe-deposit box. Bank deposits are not like that. When one brings currency to a bank for “deposit,“ the bank does not put the currency in a vault and keep it there. It may put a small fraction of the currency in the vault as “reserves,” but it will lend most of it to someone else or buy an investment--that is, a bond or some other security. As part of the inducement to depositors to lend it money, it provides facilities for transferring demand deposits from one person to another by check. The deposits of commercial banks are assets of their holders but liabilities of the banks. The assets of the banks consist of “reserves”--currency plus deposits at other banks--and “earning assets”--loans plus investments in the form of bonds and other securities. The reserves are only a small fraction of the aggregate deposits. Initially, in the history of banking, the amount of reserves held was determined by each bank separately in terms of its judgment of the likely demands on it. The growth of deposits enabled the total quantity of money (including deposits) to be larger than the total sum available to be held as reserves. A bank that received, say, $100 in gold might add $25 to its reserves and lend out $75. But the recipient of the $75 loan would spend it. Some of those who received gold this way would hold it as gold, but others would deposit it in this or in other banks. If, for example, two-thirds was redeposited, some bank or banks would find $50 added to deposits and to reserves and would repeat the process, adding $12 1/2 to its reserves and lending out $37 1/2. When this process worked itself out fully, total deposits would have increased by $200, bank reserves would have increased by $50, and $50 of the initial $100 deposited would have been retained as “currency outside banks.” There would be $150 more money in total than before (deposits up by $200, currency outside banks down by $50). Although no individual bank created money, the system as a whole did. This multiple expansion process lies at the heart of the modern monetary system. Cybercurrencies operate in a slightly different fashion to increase its coin supplies. An independent computer network uses a complex security software program which allows the creation of secured, encrypted digital “coins,” and those who create these digital coins receive a commission for services rendered in the form of new digital coins. This creation of a new medium of exchange is outside the realm of government mints and printers; it takes governments and their monetary policies out of the equation.

Governments and nations will not want to give up control of money. That control is economic power over the people. Struggles with currency and coinage was a continuing issue throughout American history. In early U.S. history, a loose political coalition of popular politicians such as Patrick Henry who unsuccessfully opposed the strong central government envisioned in the US Constitution of 1787 and whose agitation led to the addition of a Bill of Rights. The first in the long line of states'-rights advocates, they feared the authority of a single national government, upper-class dominance, inadequate separation of powers, and loss of immediate control over local affairs. Stilling their opposition in order to support the first administration of President George Washington, the Anti-Federalists in 1791 became the nucleus of the Jeffersonian Republican Party (subsequently Democratic-Republican, finally Democratic) as strict constructionists of the new Constitution and in opposition to a strong national fiscal policy. Prominent Americans such as Thomas Jefferson and Andrew Jackson have argued and fought against the central banking polices used throughout Europe. They were against the means of a government borrowing from its own people to support a vast and expensive federal government bureaucracy. A note issued by a central bank, such as the Federal Reserve Note, is bank currency. These notes are given to the government in exchange for an interest-bearing government bond. The primary means to pay for the interest on these bonds is to borrow more bank notes, thus beginning a vicious cycle that ultimately ends with the complete destruction of the currency and bankruptcy of the nation. History is replete with such occurrences. This begs the question as to why such a doomed system would exist? The reason is that during the course of the arrangement, which can last for centuries, the central bankers who issue the money amass great fortunes from the large sums of interest collected. In essence it is a transfer of wealth from the many to the elite few. Government leaders prefer such a system because it does not require budgets to be balanced. It is far more politically expedient to borrow, then to directly tax the citizens. The effects of currency debasement and debt accumulation are not obvious and in the words attributed to Vladimir Lenin by John Maynard Keynes, “By a continuing process of inflation, governments can confiscate, secretly and unobserved, an important part of the wealth of their citizens. . . There is no subtler, no surer means of overturning the existing basis of society than to debauch the currency. The process engages all the hidden forces of economic law on the side of destruction, and does it in a manner which not one man in a million is able to diagnose.” Throughout the history of the United States there has been a struggle between central bankers and their interest-bearing money and those who oppose them. In fact, the United States was created as a direct result of that struggle. The struggle for American monetary independence started very early. England sought to heavily tax the colonies in America. In 1742, the British Resumption Act required that taxes and other debts be paid in gold. As a result of scarcity of gold, the colonists turned to alternative forms of money including wampum, tobacco, and copper coins. Most silver coinage in circulation came from Spanish America, Spain, the Netherlands, the German States, France and other foreign countries. The colonies began issuing their own scrip that was paper fiat currency not backed by gold or silver. This type of money was also known as colonial bills of credit. This radically differed from the bills of debit issued by the central banks of Europe. “That is simple. In the colonies we issue our own money. It is called 'ÔColonial Scrip'. We issue it in proper proportion to the demands of trade and industry to make the products pass easily from the producers to the consumersÉIn this manner, creating for ourselves our own paper money, we control its purchasing power, and we have no interest to pay to no one.” In response, the Bank of England influenced the British Parliament to put a stop to this activity. Under the Currency Act of 1764, King George III decreed that the Colonists cease printing their own money. The colonial scrip in circulation was to be exchanged at a two-to-one ratio with notes drawn from the Bank of England. This caused widespread unemployment and economic depression in the colonies. “In one year, the conditions were so reversed that the era of prosperity ended, and a depression set in, to such an extent that the streets of the Colonies were filled with unemployed,” said Benjamin Franklin. Additional British legislation further angered the colonists who protested against taxation without representation. The Stamp Act of 1765 was the first direct tax levied by the British Parliament on the colonies. Every item of commerce - --newspapers, almanacs, pamphlets and official documents, even decks of playing cards --- were required to have the stamps. An economic boycott of British goods later led to its repeal. The Townsend Acts of 1767 placed a tax on a number of essential goods including paper, glass and tea. On April 12, 1770 all the taxes, except for that on tea, were repealed. Increased British military presence in the colonies further reduced Colonial support towards Britain. On March 5, 1770, a large boisterous mob armed with sticks of firewood began throwing snowballs and debris at a group of British soldiers. One of the soldiers was struck down and in the confusion the British soldiers discharged their muskets into the crowd. Eleven people were hit of which three were killed instantly. Two later died from their wounds. The event became known as the Boston Massacre and was often cited and exaggerated to elicit further discontent towards the British, and led to the American revolution. But the revolution did not sever the ties to old European systems. The first attempt to set up a European style central bank was the formation of the Bank of North America by Robert Morris who used gold loaned from France as a reserve deposit. Using the system of fractional reserve banking, money was loaned out to eager American political leaders who were cash-strapped from the War of Independence. Fractional reserve banking is a time-honored tradition beginning with the English goldsmiths of 1000 A.D. The goldsmiths, who at that time functioned as early bankers, discovered that they could lend out more in paper receipts for gold than they had of the actual metal so long as the majority of depositors never asked for their gold back. Fractional reserve banking is the tolerated, and now institutionalized, practice of banks lending out money they donÕt have and charging interest on it. In any other industry, this would be considered fraud. To illustrate the process, consider a bank having $1 million in reserve deposits. Under a reserve ratio of 10%, that bank may legally lend out $10 million in loans. At a modest interest rate of 7%, this equates to an annual revenue of $700,000 from an underlying asset of just $1 million. It is through this fraudulent practice that banking is such a profitable business and why all the tallest buildings in major urban centers are owned by banks. The large issue of bills from the Bank of North American led to a rapid decline in their value and collapse of the bank in 1785. The interest money collected during those years did not go unnoticed. Governor Morris of Pennsylvania, one of the authors of the Constitution of the United States, stated in 1787 that, the rich would enslave the poor through a centralized banking system. The Bank of the United States was conceived in 1790 to deal with the war debt and to put the government on sound financial footing. It was intended to help fund the government's debt and issue currency notes. Alexander Hamilton, then President George Washington's Treasury secretary, was the architect of the Bank, which he modeled after the Bank of England. The Bank was to have start-up capital of $10 million, financed by selling stock. This was quite a large sum at the time. The federal government would own $2 million, giving it substantial control, with the remainder owned by private investors. In addition to the main office in Philadelphia, the Bank had eight branches, one in each of the nation's major cities. Though the intent of the Bank was to facilitate government finances, Hamilton had another goal in mind---to function as a commercial bank. At the time of the revolution, there were barely any banks in the colonies; Britain had used its authority to protect its own banks and prevent the development of financial rivals. Hamilton's vision was to create a central source of capital that could be lent to new businesses and thereby develop the nation's economy. So while in some ways the First Bank prefigured the Federal Reserve, it also differed from it significantly by offering commercial loans, which the Fed, along with most modern central banks, does not do. The Bank can be largely judged a success both in paying off war debts and in its commercial operations, which were much larger than its public activities. However, from the beginning, there were those who argued that the Bank was unconstitutional. The Constitution granted power to tax and print money to Congress, not a private corporation, critics argued. Also, with the war debt largely taken care of, many no longer saw the need for a national bank. So in 1811, when faced with the decision to renew the Bank's charter, Congress refused, by one vote, to renew it, and the bank ceased operations. Six years after the collapse of the Bank of North America, bankers in Europe installed a private central bank, known as the [First] Bank of the United States. The bank bill was officially proposed by Hamilton, Secretary of the Treasury, to the first session of the First Congress in 1790. Coincidentally, one of HamiltonÕs first jobs after graduating from law school in 1782 was as an aide to Robert Morris, the head of the Bank of North America that collapsed in 1785. Secretary of State Thomas Jefferson argued that the Bank violated traditional property laws and that its relevance to constitutionally authorized powers was weak. He said, “I believe that banking institutions are more dangerous to our liberties than standing armies É If the American people ever allow private banks to control the issue of their currency, first by inflation, then by deflation, the banks and corporations that will grow up around (the banks) will deprive the people of all property until their children wake-up homeless on the continent their fathers conquered. The issuing power should be taken from the banks and restored to the people, to whom it properly belongs.” Hamilton argued that the while the Constitution states that while no single state government can create paper currency, there is no wording preventing the federal government from doing so. In the end, George Washington signed the bank bill into law on April 25, 1791 for a 20-year charter. In the first five years of operation, the American government borrowed $8.2 million and prices rose by 72%. “I wish it were possible to obtain a single amendment to our Constitution Ð taking from the federal government their power of borrowing.” Jefferson said in 1798. Twenty years later, the Democratic-Republican majority in Congress voted against renewing the Federalist conceived institution and the [First] Bank of the United States officially closed its doors on March 3, 1811. But the constant need for government actions to finance wars led to new forms of government loans. The War of 1812 resulted in the first significant issue of treasury notes from the United States of America. These notes differed from bank notes because they were not exchanged for an interest-bearing government bond. The US Constitution defines a difference between legal currency and bills of credit. As a result the treasury bills were not to circulate as currency and could only be issued to persons who Ômay chooseÕ to accept them. A resolution in 1814 seeking to make the treasury notes “legal tender in all debts due” was voted down 95 to 42. Some 50 years later, Congress would not demonstrate such wisdom again. Due to the costs of war, many banks had over-issued their currency from making loans to the government. In order to protect the banking industry, Congress suspended redemption of paper money in gold or silver. Instead of just keeping merely the banks solvent, this measure allowed them to further lend money. Soon the entire US banking system was in chaos. The banking system would ultimately be required to honor their obligations. This would result in widespread bankruptcies, as loans would be need to be called in to cover depositor withdrawals. The most politically viable option to prevent this was to establish a central bank to function as the lender of last resort. The Second Bank of the United States was chartered in 1816 under the administration of US President James Madison. It was founded with a mandate similar to that of the previous [First] Bank of the United States whose charter had expired five years prior. These mandates were to issue currency, purchase government debt, and serve as the official depository for Treasury funds. The bank was to raise $7 million in as reserves but never acquired more than $2.5 million. In 1818, the Bank had $2.36 million in reserves, and $21.8 million of notes and deposits on record giving it a reserve ratio of 0.11. Within one and half years the bank had added $19.2 million to the NationÕs money supply thus sparking an economic boom. As a result of soaring prices from currency devaluation the bank became in danger of being unable to honor redemptions on its reserves. To prevent such a calamity, the bank decreased the money supply from $21.9 million to $11.5 million. The 47% reduction in money supply led to a text-book example of a deflationary bust caused by manipulation of the money supply. President Andrew Jackson was an advocate of sound monetary policies as outlined in the US Constitution. He opposed the central bank system of issuing currency against debt. Jackson had an investigation done on the Second Bank of the United States which he said established “beyond question that this great and powerful institution had been actively engaged in attempting to influence the elections of the public officers by means of its money.” Jackson was a populist. Americans, especially in rural areas, distrusted Eastern bankers. In 1832, JacksonÕs re-election slogan was “JACKSON and NO BANK!” On July 10, 1832 President Jackson vetoed Congress' decision to renew the charter of The Second Bank of The United States. “It is not our own citizens only who are to receive the bounty of our government. More than eight millions of the stock of this bank are held by foreignersÉ is there no danger to our liberty and independence in a bank that in its nature has so little to bind it to our country? É Controlling our currency, receiving our public moneys, and holding thousands of our citizens in dependenceÉ would be more formidable and dangerous than a military power of the enemy,” Jackson said as he vetoed the bill. In 1833, President Jackson instructed his Secretaries of the Treasury to cease depositing funds to the bank. Two refused to obey, so he fired them, one after the other, until he got one who did: Roger B. Taney, his former Attorney General and the future Supreme Court Chief Justice. In 1835, Jackson paid off the final installment on the national debt. He was the first and only president to ever accomplish this. But history repeats itself; this time it was the Civil War. In order to finance the NorthÕs Civil War efforts, Lincoln approached the European banks controlled by the Rothschilds in 1861. They demanded 24% to 36% interest. Lincoln refused and instead passed the Legal Tender Act of 1862. Under this new piece of legislation, Lincoln issued US$449,338,902 of interest-free money, known as “Greenbacks,” so-called from the green ink they used. It served as legal tender for all debts, public and private and was used to finance the UnionÕs Civil War efforts. “The government should create, issue and circulate all the currency and credit needed to satisfy the spending power of the government and the buying power of consumers É The privilege of creating and issuing money is not only the supreme prerogative of Government, but it is the GovernmentÕs greatest creative opportunity. By the adoption of these principles, the long-felt want for a uniform medium will be satisfied. The taxpayers will be saved immense sums of interestÉ”said Lincoln. By the end of 1863, Congress had authorized the printing of US$850 million worth of Greenbacks. Private banks used these Greenbacks as bank reserves, against which the issued their own bank notes and demand deposits. Over the course of the US Civil War the money supply went from $45 million to $1.77 billion. Prices subsequently skyrocketed. In 1863, Congress passed the National Bank Act from which point forward, all money in circulation would be created out of debt from bankers buying US government bonds in exchange for bank notes. By 1865, the national banks had 83 percent of all bank assets in the United States. In the intervening 70 years since the Second Bank closed, central banks in other countries such as England began to take on new roles. Their preferred status as the government's banker caused others to view them as more secure, which led to their holding deposits and serving as a “banker's bank.” That, along with an expanded role in payments and lending, led to their taking on a regulatory role, since they needed to ensure the quality of banks with which they were doing business. And finally, their power over the issuing of currency and tremendous capital holdings led to the development of monetary policy, for which central banks are now best known. In designing the new Bank lessons were taken from the First and Second banks. They removed the private role of the bank in commercial lending, so that the new bank would be a largely public institution. Profits in excess of cost were handed over to the US Treasury. In addition, the Fed was given authority over the nation's payments system. Financial transfers and check processing that were handled by private clearinghouses would now be conducted by the Fed, with the fees for such services going to run the Bank. Wary of repeating political battles, the Federal Reserve's founders designed a decentralized central bank to prevent the concentration of power. There was concern that the new central bank would be run by, and for, Wall Street, and so it was important to the founders that the Bank not be focused on New York. Thus, the system was decentralized into District Banks, which operated independently, and with an oversight board located in Washington, D.C. Each District Bank issued its own money, backed by the promise to redeem this money in gold. After Congress passed and President Woodrow Wilson signed the Federal Reserve Act in 1913, Congress established 12 District Banks to reflect the distribution of population and banking in the country. Today, what the Federal Reserve is best known for is monetary policy, but that was not an original role of the institution. New York Fed President Benjamin Strong began conducting open market operations in the 1920s. Many historians blame the Fed's botched monetary policy for the length and severity of the Great Depression. But it was when President Franklin Roosevelt took the nation off the gold standard in 1933 that monetary policy really matured. Now that the nation was explicitly using fiat money for the first time, a formal authority became necessary to ensure that policy would be carried out responsibly. In 1935, Congress created the Federal Open Market Committee, to be the Fed's monetary policy arm. Like its predecessors, the Federal Reserve has had a sometimes stormy relationship with the executive office and Congress over the years. The federal government took more control of the Federal Reserve during the Great Depression and World War II, but since 1951---and the resolution of a power struggle with the Treasury Department--- the central bank has operated largely independent of the political process. Still, the Federal Reserve regularly reports to Congress and must answer questions and address issues important to the House and the Senate. This System, an independent central bank, has become a model for countries around the world. Distrust for a centralized government bank is not new. People can clearly remember the 2007 financial crisis that destroyed the housing and financial markets in the United States. But there are other examples throughout history, normally called "panics" as banks getting themselves into trouble, unable to meet their legal obligations. Three failed attempts of establishing a central bank in the United States did not dissuade a fourth. By the beginning of the 20th century the most influential business men and bankers were the J.D. Rockefeller, J.P. Morgan, Paul Warburg, and the Rothschilds. The Panic of 1907 was a run on the American banking system as a result of a public announcement by JP Morgan that a prominent bank in New York was insolvent. The results were wide-spread mass withdrawals on the entire banking system. These depositor bank runs forced the banks to call in their loans. Bankruptcies, repossessions and financial turmoil emerged. Congress created the National Monetary Commission after the Panic of 1907 to draft up a plan for banking reform. Nelson Aldrich headed the Commission that comprised of two components--- one to study the European central banking systems headed by Aldrich himself and another to study the American monetary system. Centralized banking was met with much opposition from the American public, who were suspicious of a central bank and who charged that Aldrich was biased due to his close ties to wealthy bankers such as JP Morgan and his daughterÕs marriage to John D. Rockefeller, Jr. The purpose of the Federal Reserve Act was to transfer control of the money supply of the United States from Congress as defined in the US Constitution to the private banking elite. The deceptive terminology of the name was carefully chosen because the American public did not want a central bank similar to those in Europe. The Federal Reserve is not a federal governmental entity nor is it a reserve, such as a governmental treasury, backing up its currency. The Federal Reserve is a legalized cartel of the money supply owned by private national banks, operating for the benefit of the few under the guise of protecting and promoting public interests. The meeting on Jekyll Island remained unknown to the public until Forbes magazine founder Bertie Charles Forbes wrote an article about it in 1916, three years after the Federal Reserve Act was passed. Wilson wrote in his book, The New Freedom: “A great industrial nation is controlled by its system of credit. Our system of credit is privately concentrated. The growth of the nation, therefore, and all our activities are in the hands of a few men É [W]e have come to be one of the worst ruled, one of the most completely controlled and dominated, governments in the civilized worldÐno longer a government by free opinion, no longer a government by conviction and the vote of the majority, but a government by the opinion and the duress of small groups of dominant men.” A central banking system wherein every dollar created is an instrument of debt requires the collection of large sums of money from the people to pay off the interest. Interestingly, 1913 was also the year that introduced the Sixteenth Amendment, thereby giving government the power to collect taxes based on income, which in theory should have lessened the need of the government to borrow money to pay its debts. But this did not stop additional panics and the Great Depression. Under the pretense of helping to end the Great Depression came the 1933 Gold Seizure mandate whereby the Roosevelt Administration outlawed private ownership of gold. Under the threat of imprisonment for 10 years, a US$10,000 fine or both, everyone in America was required to turn in all gold bullion to the US Treasury. The rationale for the seizure was that the declining prices of the Great Depression were a direct result of overcapacity. This flawed reasoning resulted in the creation of disastrous policies such as National Industrial Recovery Act where business cartels were deliberately constructed to keep prices high and the Agricultural Adjustment Act that ordered mass destruction of livestock and crops in order to reduce supply and drive up prices. In a time when unemployment is at record highs and people are suffering from economic hardship, these policies are the complete opposite of what is required. As a final component to the Roosevelt AdministrationÕs desire to increase prices was to devalue the dollar. To do so required that the dollar be uncoupled from gold. As long as the dollar was tied to a gold standard, the amount of money in circulation could not dramatically increase as the public would convert the paper into gold when they became aware of the over-issuance of paper currency. On April 5, 1933, Roosevelt signed Executive Order 6102, which ordered people to turn in their gold to the government at payment of $20.67 per ounce. Individuals could hold up to $100 in gold coins, and there were some exceptions for dental use, jewelry, and artists and others who used gold in their jobs. While US citizens could be ordered not to hoard gold, Roosevelt knew he could not impose such a law on sovereign nations. Foreigners could still exchange there US dollars for gold, but shortly after issuing Order 6102, Roosevelt devalued the dollar to US$35 per ounce thereby decreasing the value of the dollar overnight by 40.94%. The result of these policies allowed greater ability of the Federal Reserve to increase the amount of money in circulation thereby increasing their revenue from interest. Another war, Vietnam, also changed the American monetary system. Escalating costs from both the Vietnam War and domestic social programs resulted in ever increasing amounts of US dollars being printed. In the early 1970''s, the United States as a whole began running a trade deficit for the first time in the 20th century. Foreign owners of US dollars began to question the ability of the US government to reduce budget and trade deficits. Increasingly, foreign nations, in particular the French under Charles de Gaulle, began to send the US dollars earned by exporting to the US back to be redeemed in gold as legally entitled under the Bretton Woods Agreement signed in 1944. The drain on US gold threatened to completely empty the US Treasury. To prevent this from happening, on August 15, 1971, President Richard Nixon unilaterally closed the gold window. He made the dollar inconvertible to gold directly, except on the open market. The severing of this last link between gold and paper money meant that all the worldÕs currencies now “floated” against one another. The result was inevitable with gold soaring from US$35 to US$195 an ounce by the end of 1974. This was the final step in abandoning the gold standard. All the central banks had to control now was the public's perception of inflation to allow them to create as much money as desired. On January 1, 1975, after 42 years, it became “legal” for individual Americans to own gold again. Anticipating the demand, many central banks sold off large quantities of their gold reserves. The effect was a decline in the price of gold to US$103 a troy ounce in eighteen months. The vicious cycles of high debt, high interest rates and inflation continued deep into the century. Fed Chairman, Paul Volcker, appointed by Jimmy Carter, announced a change in policy upon return from a conference in Belgrade concerning the global financial system. He announced that the US Federal Reserve was switching its policy from controlling interest rates to controlling the money supply. But a growing supply of money creates bubbles in the markets, whether it be stocks, bonds, mortgages, houses or commodities. Further fueling the rise in equities was the effective abandonment of the permanent debt ceiling of US$400 billion set in March 1971. By late 1982, the public debt had tripled to US$1.25 trillion. Presently, the public debt of the United States stands at more than US$16.5 trillion. This explosion of debt led to worldwide monetary inflation as the US still enjoys a “de facto” reserve currency status by virtue of history and an agreement made with OPEC in 1973 that world oil would be priced in US dollars. (But other emerging nations, such as China, want to remove the United States dollar as the international means of exchange.) Monetary inflation leads to the formation of economic bubbles wherein market speculators bid up the prices of assets to unrealistic highs. When all market participants have clambered into the market the market generally collapses when it becomes apparent that there is nobody left to buy. The current Federal Reserve banking system is modeled after the European central banking system Americans revolted against during their War of Independence. Every dollar created under the present monetary system does not represent a tangible asset. It represents an illusory “ I.O.U.” from the government, and therefore the people, to the central bank. After three failed attempts, central bankers finally gained control the monopoly on the issuance of American money with the creation of the Federal Reserve in 1913. There are two unavoidable results of the Federal Reserve System: (1) devaluation of the dollar and (2) accumulation of debt. Every dollar created is an instrument of debt lent out at interest. The extra money required to pay back the interest can only come from one place, that being the central bank. As such, the central banks must continuously increase the money supply. At some point, the public begins to question the fiction of government money as having any true value (such is the case during hyperinflation in South American countries when their economies collapse). So may people believe there has to be a better way to transact commerce, especially in this computer age. But forming a new integrated system of digital exchange is not easy since it does not have a standardized banking structure to facility quick and easy payments and credits with trusted accounting. The first concern of a central bank is the maintenance of a soundly based commercial banking structure. While this concern has grown to comprehend the operations of all financial institutions, including the several groups of nonbank financial intermediaries, the commercial banks remain the core of the banking system. A central bank must also cooperate closely with the national government. Indeed, most governments and central banks have become intimately associated in the formulation of policy. Central banks have over the years acquired a number of well-defined responsibilities to their respective national governments. Some, notably the Bank of England, developed into central banks after being, in origin, bankers to the government. More recently it has become a matter of course for a new central bank to accept responsibility for the financial affairs of its government. The reasons are self-evident. Government transactions have become of increasing importance in influencing the workings of the economy, and the institution that holds the government's account is in a strategic position to cushion the commercial banks against the impact of large movements of cash originating in this way. As banker to the government, furthermore, the central bank has an obvious responsibility to provide routine banking services, such as arranging loan flotations and supervising their service, renewal, and redemption. The central bank also usually issues the currency. Equally important are its responsibilities as an adviser on the probable monetary consequences of any proposed action. In this role the central bank should scrutinize the government's proposals with a certain amount of objectivity and state its point of view with vigor. One may cite a now-famous dictum of Montagu Norman as governor of the Bank of England: “I think it is of the utmost importance that the policy of the Bank and the policy of the Government should at all times be in harmony--in as complete harmony as possible. I look upon the Bank as having the unique right to offer advice and to press such advice even to the point of 'nagging'; but always of course subject to the supreme authority of the Government.” Many central banks are now nationalized, reflecting the increasingly general recognition of the significance of the central bank's role as a servant, if not a creature, of the government. This development is also, in a way, a final recognition of the central bank as a responsible public institution whose major function is to serve the community as a whole, untrammeled by narrow dictates of profit and loss. Most central banks, nevertheless, make very handsome profits. There will always be those who will try to get around the influence of a central bank. In US history, an 1836 executive order issued by President Jackson required that payment for the purchase of public lands be made exclusively in gold or silver. It was Jackson's effort to curb excessive land speculation and to quash the enormous growth of paper money in circulation, Jackson directed the Treasury Department, “pet” banks, and other receivers of public money to accept only specie as payment for government-owned land after Aug. 15, 1836. But actual settlers and bona fide residents of the state in which they purchased land were permitted to use paper money until December 15 on lots up to 320 acres. The Specie Circular, by seriously curtailing the use of paper money, was highly deflationary and at least in part produced the ensuing credit crunch and the economic crisis called the Panic of 1837. On May 21, 1838, a joint resolution of Congress repealed the Specie Circular. “The Ohio Idea” was a proposal first presented in the Cincinnati Enquirer in 1867 and later sponsored by Senator George H. Pendleton of Ohio to redeem American Civil War bonds in paper money instead of gold. The Ohio Idea was part of the struggle between hard-money (specie) and soft-money (greenback) advocates during the post-Civil War era. Backers of the Ohio Idea were people who would benefit from inflation, and the proposal was endorsed in the Democratic platform of 1868. It was especially popular in the Midwest. Once Ulysses S. Grant was inaugurated as president, however, the Ohio Idea quickly died. The Public Credit Act of March 18, 1869, provided for payment of government obligations in gold. The Resumption Act of 1875 was the culmination of the struggle between “soft money” forces, who advocated continued use of Civil War greenbacks, and their “hard money” opponents, who wished to redeem the paper money and resume a specie currency. By the end of the Civil War, more than $430 million in greenbacks were in circulation, made legal tender by congressional mandate. After the Supreme Court sanctioned the constitutionality of the greenbacks as legal tender, hard money advocates in Congress pushed for early resumption of specie payments and retirement of the paper money. On Jan. 14, 1875, Congress passed the Resumption Act, which called for the Secretary of the Treasury to redeem legal-tender notes in specie beginning Jan. 1, 1879. The bill also called for reducing the greenbacks in circulation to $300 million and for replacing the fractional paper currency (“shinplasters”) with silver coins as rapidly as possible. Members of the new Greenback Party were bitterly opposed to the Resumption Act, and in 1878 they succeeded in raising the amount of paper money allowed in circulation. Specie resumption proceeded on schedule, however, and Treasury Secretary John Sherman accumulated enough gold to meet the expected demand. When the public realized that the paper money was “good as gold,” there was no rush to redeem, and greenbacks continued as the accepted currency. (And this is the one truth of any currency: it's value is determined by people's perception of its worth.) The same debates Alexander Hamilton and Thomas Jefferson had over a central bank are relevant today. The idea of a central government fiscal policy and funding of massive public debts are contrasted by the fact that the market system needs to facilitate the issuance of a stable national currency, and to provide a convenient means of exchange for all the people of the United States. However, in the last nine years, the true economic value of an American dollar has more than 34 percent, due to the high federal deficits. Just as some claimed that the gold standard could not sustain the required economic growth of the nation, many claim today that the massive state, federal and local government debts will continue to choke the nation's economy as small business and individual taxpayers do no have the means to pay for their government's excess behavior. The cycle of government borrowing, money oversupply, high debts, leveraged investments, and market bubbles have led many people to seek alternative means of exchange and trade. Legendary investor Jim Rogers, who delivered his frightening warning recently on Yahoo! Finance. Rogers believes we are heading for a massive collapse of the dollar which will cause interest rates to soar to record levels. He warned investors should stay clear of the dollar and other fiat currencies. “There is no sound currency anymore,” Rogers stated. “There's no paper money in 2014 and 2015 that's going to be worth much of anything,” he added. According to Bloomberg, the US dollar has indeed reached a startling two-year low--- its weakest since November 2011--- with consumer confidence dropping like a rock. And the US dollar has lost 38.5% of its value since 2002. “For the first time in recorded history we have all major banks and central governments around the world printing huge amounts of money,” Rogers said. “This has never happened in world history and so the world is floating on an artificial ocean... of lots and lots of printed money," said Rogers. Rogers noted that the situation will only get worse if the government continues to 'kick the can down the road.' When the can goes over the road, we're all going to go with it. The debt is going higher and higher. The money printing is going higher and higher. We've had 50 or 60 years of success in America,” Rogers said. “You've got to pay the price someday whether you like it or not. The longer you delay the day of reckoning, the worse the day of reckoning is going to be. This is not going to be fun.” He added that the problems will not be solved with the Federal Reserve intact. “Abolish the Federal Reserve,” Rogers stated. “The world has gotten along quite famously and well without central banks for most of world history. America has had three central banks in our history, the first two disappeared,” he said. “This one's going to disappear too because they keep taking on huge amounts of debt... they keep leveraging up the balance sheet... they keep making mistake after mistake... they're printing money, it's going to self-destruct before it's over.” Rogers argues that we would be better off with no central bank than the current Federal Reserve system. Rogers predicts that Americans will soon abandon the dollar and seek an alternative currency, such as Bitcoins. However, Wall Street investment bank Goldman Sachs does not believe alternative currencies are currencies. The firm has put together an exhaustive survey of the technology and states Bitcoin likely cannot work as a currency, because it is not a the ledger-based technology since Bitcoin is a peer-to-peer network that allows for the proof and transfer of ownership without the need of a trusted third party. The unit of the network is bitcoin. Goldman SachsÕ analysts consider bitcoin Ñ the unit of exchange Ñ more like a commodity than a currency, according to the report. “We would argue that Bitcoin, and other digital currencies, lie somewhere on the boundary between currency, commodity and financial asset,” wrote Dominic Wilson, chief markets economist at Goldman Sachs, and Jose Ursua, a global economist with the firm. “Our best definition would be that it is currently a speculative financial asset that can be used as a medium of exchange.” A successful cyber-currency needs a fixed exchange rate to succeed, according to the economists and the difficulties Bitcoin faces as a store of value are significant obstacle to its adoption. As a tradeable commodity, Goldman Sachs says Bitcoins still will not hold a candle to the gold-standard of commodities --- gold. “A commodity is any item that 'accommodates' our physical wants and needs. And one of these physical wants is the need for a store of value,” writes Currie. Currencies, by contrast, are instruments that are secured by either a commodity or a government's ability to tax and defend. By Currie's reasoning, commodities become supplanted when a better commodity comes along, so, for him, the question is whether Bitcoin solves an economic problem that currently exists with gold. “The short answer is no. Gold is not failing as a store of value as wood failed as a sources of energy in steam engines. Steam locomotives could go farther and faster on coal. But Bitcoin does not improve upon gold.” The Internal Revenue Service has just issued a regulation that states that bitcoins are property and not a currency. The ramification of the ruling is that as property, the use and trade-in of bitcoins for dollars will cause capital gains imputed on the digital currency users. For example, if you mined a bitcoin which had the value of $100, but later used it to sell, buy or trade for an item worth $300, the bitcoin miner would have a $200 capital gain to report as income to the IRS. Another problem with alternative, digital currencies is that the means of exchange is outside the acceptable standard credit payment processing centers. Bitcoin is a digital currency that exists almost wholly in the virtual realm, unlike physical currencies like dollars growing number of proponents support its use as an alternative currency that can pay for goods and services much conventional currencies. Bitcoin is the first and easily the most popular cryptocurrency, or currency that uses cryptography to control its creation, administration and security. Bitcoin was set up in 2009 by a mysterious individual or group with the pseudonym Satoshi Nakamoto, (and Newsweek's recent article has been called into question about who this person truly is). .Bitcoin rocketed to prominence in 2013, when the value of a Bitcoin than 10-fold in a two-month period, from $22 in February to a record $266 in April. At its peak, based on more bitcoins issued, the cryptocurrency boasted a market value of over $2 billion. Bitcoin differs from conventional currencies in some very fundamental ways, as noted below (for the sake of simplicity, the US dollar as a proxy for conventional currencies). Bitcoin uses P2P technology without a central authority: Bitcoin is a decentralized currency managed peer-to-peer technology (P2P2), without a central authority. All functions such as Bitcoin issuance, transaction and verification are carried out collectively by the network, without a central supervisor or agency to oversee contrast, a conventional currency is issued by a central bank as part of its mandate to manage national monetary the US, only the Federal Reserve has the power to issue dollars; it is also the central authority that conducts policy, supervises banks, maintains financial system stability, and provides financial services to depository Bitcoin is primarily digital: Although physical Bitcoins are available from companies such as Casascius Bitcoin has been designed primarily to be a digital currency. Physical Bitcoins are somewhat of a novelty, of a tangible form defeats the purpose of a digital currency, according to the most ardent supporters of the Conversely, your dollars exist primarily in physical form; the balances that you hold at your bank and online be converted into physical dollars within minutes if you so desire. Bitcoin has a maximum 21 million limit: The total number of Bitcoins that will be issued is capped at 21 Bitcoin “mining 3 process presently creates 25 Bitcoins every 10 minutes (the number created will be halved years), so that limit will not be reached until the year 2140. While Bitcoin critics argue that the maximum enough, supporters maintain that since each Bitcoin is divisible to eight decimal places, the number of fractional (called “satoshis”) Ð at 21 x 1014 Ð will be more than enough for all conceivable applications. Conventional the other hand, can be issued without limit. Bitcoin is a complex product. The concepts of cryptocurrencies in general are abstruse and abstract, and how and why Bitcoin works requires a fair degree of technological knowledge. Bitcoin has limited acceptance so far and cannot be used at brick-and-mortar although that may eventually change if it continues to gain traction. The dollar, on the other hand, has near-acceptance as the worldÕs global reserve currency. Bitcoin transactions have limitations. A Bitcoin transaction can take as long as 10 minutes to confirm. It is also irreversible and can only be refunded by the Bitcoin recipient. These limitations do not exist with conventional currencies, where debit and credit transactions are confirmed within seconds. Bitcoin balances are not insured. This means that if you lose your Bitcoins for any reason Ð for example, drive crashes, or a hacker steals the digital wallet in which your Bitcoins are stored, or the Bitcoin exchange a balance went out of business Ð you have little recourse. Currency balances held at banks, on the other hand, against certain events such as bank failure by agencies like the Federal Deposit Insurance Corporation. Bitcoins have no such insurance. A new user needs to install a digital wallet on a computer or mobile device. This wallet is simply a free, open-source software program that will generate your first subsequent Bitcoin addresses. There are three types of wallets Ð a software wallet (installed on your computer), (which resides on your mobile device) or a Web wallet (located on the website of a service provider that hosts Bitcoin uses public key encryption techniques for security. This means that when a new Bitcoin address is created, cryptographic key pair consisting of a public key and private key Ð which are essentially unique, long strings of numbers Ð is generated. Each address has its own Bitcoins balance, so all you need to do is acquire a number of Bitcoins that will be held addresses in your wallet. You can acquire Bitcoins through a number of ways Ð by buying them from a Bitcoin currency exchange such as Mt. Gox or Bitstamp, or through a service like BitInstant that enables fund transfers between exchanges and supports various payment mechanisms. Note that all Bitcoin transactions are stored publicly and permanently on the Bitcoin network, which means that transactions of any Bitcoin address are visible to anyone. Experts therefore recommend that Bitcoin owners create address for each transaction as a means of ensuring privacy and enhancing security. Once you have created a Bitcoin address and have acquired Bitcoins, you can use them for an online transaction that accepts Bitcoins as a payment mode. The company will send you the Bitcoin address to which you can send payment. You direct the payment to that address; while the transaction takes place within seconds, verification minutes or longer. All Bitcoin transactions, without exception, are included in a shared public transaction log known as a “block chain” to confirm that the party spending the Bitcoins really owns them, and also to prevent fraud and double-spending. Why does transaction verification or confirmation take so long? Because the complex algorithms involved in Bitcoin take time to solve, even with immense computing power at oneÕs disposal. If a person wants to make an online payment to a company using 5 Bitcoins that you address in your digital wallet. The company creates a new Bitcoin address and directs you to send your payment to it. This creates a private account and a public key (available to you and anyone else). Note that just as a seller does not need physical identity if you pay cash, you do not need to disclose your real identity to the company. You instruct your Bitcoin client (the free Bitcoin software you first installed on your computer) to transfer your wallet to the company's address. This is the transaction message. Then, your Bitcoin client will electronically “sign” the transaction request with the private key of the address from transferring the Bitcoins. Your public key is available to anyone for signature verification. Your transaction is broadcast to the Bitcoin network and will be verified in a few minutes that the Bitcoins have successfully transferred from your address to the company's address. The first two steps involve action by the seller and you respectively. The latter two steps are automatically executed by the Bitcoin client software and Bitcoin network. As well, storing the private key attached to an address securely is of the utmost importance; otherwise, anyone who obtains the private key can control the Bitcoins at use them fraudulently. As the first cryptocurrency to capture the public imagination, Bitcoin has the lead on the competition. Total issuance is limited to 21 million, so it is unlikely to be devalued because of the prospect of a massive bitcoins. As a decentralized currency, Bitcoin is free from government interference and manipulation. Transaction costs are much lower than with conventional currencies. On the flip side, BitcoinÕs disadvantages include the price of a Bitcoin has been increasingly volatile, making it difficult to assess its real value and increasing losses for investors in the cryptocurrency. The relative anonymity of Bitcoin may encourage its use for illegal and illicit activities such as tax evasion, procurement, gambling and circumvention of currency controls. The fact that bitcoins exist primarily in digital form renders them vulnerable to loss. But how Bitcoins are actually created is all too often overlooked. The currency is not minted at will in a factory setting. Bitcoins don't just magically appear out of thin air. Instead, they're the products of complex software algorithms that run day and night on incredibly powerful computers. So who, exactly, has the pioneering spirit to “mine” the virtual currency, converting CPU and GPU cycles into something of real-world value? With Bitcoin gaining traction as a viable currency, more and more people are interested in mining for a piece of the digital pie. However, mining for profit is more difficult than just loading up some software and watching the cash flow in. It is not a simple task. It may take thousands of dollars to get the right equipment. Bitcoin mining requires a considerable investment (and intestinal fortitude) just to get started. Bitcoin is an electronic currency that isn't tied to any country or economy--it's decentralized. Its value is constantly changing (just like any other currency), In order to buy, trade, or use Bitcoins, the units of currency have to first be introduced to the market. And that's where miners come in. Bitcoins themselves are algorithm-based mathematical constructs, running software searching algorithm, searching for a specific chain of code. When that code is found, a block of Bitcoins is rewarded to whoever found it. Current blocks contain 25 Bitcoins, but the block size goes down by half every four years, making mining harder and less profitable as time goes on. Bitcoin miners run specialized computer setups that constantly run the mining algorithm in hopes that a block of coins will be found. Currently, there are roughly 11.4 million Bitcoins in circulation--that number will cap at 21 million in 2140, according to the algorithm's limitations. The high investment costs in high end CPUs, cooling equipment and the long time to mine bitcoins leads to rare profits for newer coin miners. The risk is like prospectors rushing to a gold strike area, only to find that they are not the first to arrive - - - and the veins are mostly gone. Further complicating the miner's potential profitability is the dramatic flux in bitcoin prices, and the lack of stability in value puts any return on investment at risk. The criminal aspect of digital coins and currency mining is growing. Bitcoins are created through a mining process where a computer's resources are used to perform millions of calculations. But since the process is a computer program, any computer program is open to hacks. Criminals can add malware to their botnets to turn infected computers into bitcoin miners. This triggered predictions of doom for bitcoin --- that the criminals would take over the mining of bitcoin through botnets and bring the whole currency crashing down. But as bitcoins become harder to mine - according to an algorithm that slows down their production the more people try to create them --- this approach has proven less profitable. In 2012-13,miners only earned at least 4,500 bitcoins, a relatively small sum compared with the total produced. So criminals are turning to stealing bitcoins from wallets, or, more lucratively, from exchanges. According to data compiled last year by academics Tyler Moore and Nicholas Christin, of 40 exchanges tracked 18 had closed, with customer balances wiped out in many cases - not always, they point out, due to fraud. Since then, according to public reports, more than a dozen others have been hacked. Reuters reports that Cyber-criminals have also made use of the ease with which bitcoins can be traded without any third party - such as a bank or online payments service like PayPal - to use it as at least one way of paying for services between themselves. “Bitcoin made it much easier for them, because they have to trust each other even less. Even complete strangers can cooperate,“ said Juraj Bednar, a bitcoin security expert in Slovakia. The US government has shut down several operations, including the Silk Road group. The use of cybercurrency to fund illegal activities such a drug sales is a concern for law enforcement. The system is supposed to allow open transparency for every transaction, but security analysts say that bitcoin services are used “launder” bitcoins to hide their origin. The big score is hacking and stealing digital coins from exchanges, like Japan's Mt. Gox, which lost hundreds of millions of dollars worth of bitcoins. For now, bitcoin users remain a vulnerable target to thieves, and not an easily used or understood means for the general public to transact business. Bitcoins do not have the acceptance of the general public; it is not gained the trust of the public to be an acceptable, stable means to dethrone the US dollar or gold as a valuable means of payment or value.

Source materials include Encyclopedia Britannica, CNet, Federal Reserve publications, DollarDaze.org, techcrunch, investopedia.com, Yahoo! Finance, ITWorld, wikipedia, and Reuters.